On 30 December 2025, the Minister of Finance (“MoF”) issued MoF Regulation No. 113 of 2025 on Excise Refunds (“MoF Reg. 113/2025”). This regulation revokes MoF Regulation No. 113/PMK.04/2008 of 2008 on Excise Refunds and/or Administrative Sanction in the Form of Fines (“MoF Reg. 113/2008”). While the objectives and contents of MoF Reg. 113/2025 are broadly similar to those of MoF Reg. 113/2008, MoF Reg. 113/2025 provides further clarification on the procedures for excise refunds.

In this article, we highlight key provisions that business owners should consider in relation to claiming an excise refund to the Directorate General of Customs and Excise (“DGoCE”) under MoF Reg. 113/2025.

Conditions for Excise Refunds

The qualification for excise refunds remains largely unchanged from those under MoF Reg. 113/2008. In particular, the conditions of the goods to be eligible for excise refunds are generally consistent with the ones under the previous framework. Under Article 2(2) of MoF Reg. 113/2025, goods are eligible for excise refund if they fall into any of the following conditions:

- the goods’ excise has been paid by way of affixing excise stamps, provided that the stamps are ordered in the current fiscal year and/or in the immediately preceding fiscal year; or

- the goods’ excise has been paid by way of payment settlement, provided that the excise is paid in the current fiscal year and/or in the immediately preceding fiscal year.

Entitled Parties

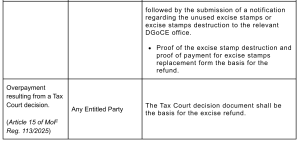

MoF Reg. 113/2025 stipulates different types of excise refunds and identifies the parties entitled to apply for them. In particular, the regulation refers to the following entities: (i) manufacturers; (ii) importers of excisable goods; (iii) storage business operators; or (iv) other parties as determined by a Tax Court decision (collectively referred to as “Entitled Party”).

Further, the regulation identifies the Entitled Party as those eligible to apply for excise refunds, subject to the satisfaction of the refund conditions. The table below summarises the foregoing:

Refund Mechanism

MoF Reg. 113/2025 further clarifies the refund mechanism, not expressly addressed in the earlier regulation. Under Article 16 of MoF Reg. 113/2025, an excise refund is granted to the Entitled Party based on the relevant refund document, provided that: (i) the excise payment for the refund is recorded in the state treasury; and (ii) the refund request is made within 10 years from the date of issuance of the relevant underlying refund document.

The refund is granted after being set off against the Entitled Party’s outstanding excise liabilities. If the Entitled Party has no outstanding excise liabilities, it may use the refund for either: (i) settlement of future excise liabilities; and/or (ii) cash refund.

Where the Entitled Party intends to use the refund to settle future excise liabilities, it must notify the head of the relevant DGoCE office of that intended use. By contrast, a refund arising from a Tax Court decision may only be made in cash.

MoF Reg. 113/2025 also formalizes the electronic refund mechanism, reflecting existing practice. Refund applications may now be submitted online through the dedicated system established by DGoCE, CEISA 4.0.(https://portal.beacukai.go.id/).

Concluding Remarks

MoF Reg. 113/2025 reflects a measured refinement of Indonesia’s excise administration by preserving the substantive grounds for excise refunds, while providing greater procedural clarity on how such refunds may be claimed, evidenced, and applied, including through electronic filing. Rather than materially expanding the scope of entitlement, the regulation appears primarily to clarify the regulatory framework surrounding that entitlement, including who may apply, in what circumstances, on the basis of which documents, and subject to what temporal and administrative constraints. For businesses operating in excisable sectors, the regulation accordingly underscores the practical importance of compliance, since the success of an excise refund claim may depend not only on the existence of a qualifying event, but also on the claimant’s ability to demonstrate procedural accuracy, documentary completeness, and alignment with the statutory mechanism prescribed by DGoCE.

Disclaimer: The information herein is of general nature and should not be treated as legal advice, nor shall it be relied upon by any party for any circumstance. Specific legal advice should be sought by interested parties to address their circumstances.